{kind=link}

India, known as the second-largest producer of vegetables and fruits in the world, after China, relies heavily on fertilisers to sustain its agricultural output. The 2025 GST reforms marks a significant step by the government to support farmers in agriculture and food production. These measures ensure ease in input costs and boost domestic competitiveness.

GST Reforms 2025 Overview:

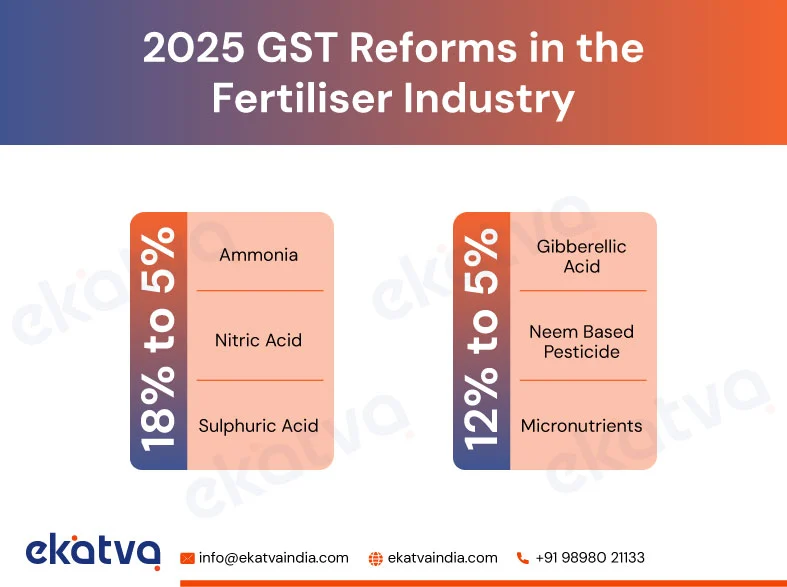

The Government, through the 56th GST Council Meeting, announced a tax reduction from 12% or 18% to 5% for the fertiliser sector. Products such as gibberellic acid, micronutrients, and neem-based pesticides are available at 5% GST rate, effective from September 22, 2025. Further, GST on ammonia, sulphuric acid, and nitric acid have also seen a reduction from 18% to 5%. The rate rationalisation suggested a mild cheer for farmers and in the inclusive supply chain, resulting from cheaper rates and removal of duty inversion.

Impact of GST Reforms on the Fertiliser Industry:

Previously, manufacturers in the fertiliser industry were burdened with high GST on inputs and low GST on sales, creating an inverted duty structure. It leads to disruption in working capital and disregard for the system in low sales. However, the GST reforms led to a reduction in the input tax, and manufacturers find relief with the present working capital.

Suppose the input cost of manufacturing fertilisers is Rs 2,700,000 with 18%/12% GST on the cost value, i.e., Rs 468,000, resulting in the total cost of fertilisers to be Rs 3,168,000. Now, the manufacturer sells it at an estimated cost of Rs 3,000,000 to earn Rs 300,000 as profit. The GST on the sale of fertiliser is at 5% which equals Rs 150,000, resulting in Rs 3,150,000 as the total sale value.

With the GST reforms, the tax rate was reduced from 18%/12% to only 5% on input costs. The change in GST tax rates led him to pay only Rs 135,000 on the cost price, keeping other values the exact same. The larger input tax than the output tax previously resulted in an inverted duty structure and a claim for Rs 318,000. However, the GST reforms ensured no inversion, with input tax less than the output tax, with a difference of Rs 15,000.

Particulars | Before GST Reform (₹) | After GST Reform (₹) |

|---|---|---|

Selling Price (A) | 3,000,000 | 3,000,000 |

GST on Sale (B) | 150,000 (5%) | 150,000 (5%) |

Total Sale Value (A + B = C) | 3,150,000

| 3,150,000

|

Cost Price (C) | 2,700,000 | 2,700,000 |

GST on Cost (D) | 468,000 (18%) | 135,000 (5%) |

Total Cost Value (C+D) | 3,168,000 | 2,835,000 |

Profit (B-D) | 300,000 | 300,000 |

Inverted Duty Structure (B-D) | -318,000 | 15,000 |

The vision of Shri Narendra Modi, “One Nation, One Market, One Tax”, has led to standardisation in the tax structure for businesses in the fertiliser sector in India. It further leads to an easy claim of Input Tax Credit (ITC) for these businesses, because of the difference in GST amount. The reformed tax structure benefited farmers more than anyone else, with reduced burden of taxation and increased productivity with effective utilisation of fertilisers. Moreover, it also enhanced compliance with smoother cash flows and optimal use of working capital.

However, certain issues still persist in the fertiliser industry, such as higher GST rates on conventional pesticides, delays in processing ITC refunds, and blocked credits for subsidised products. The Next Gen GST reforms acknowledge the barriers and have successfully addressed issues with working capital, which has significantly led to the rise of MSMEs and farmers in India. With this, it aims to create a driving force for competitiveness, self-reliance and sustainable growth of the fertiliser industry while also enhancing liquidity.

Inverted Duty Structures Maybe Hindering Your Profits.

We help you with maintaining proper working capital and ITC claims.