Published On:

Updated On:

{kind=link}

The government’s focus on welfare in the education sector has taken the next move from exempting GST from school and university education to making learning materials affordable. The simplified GST structure consists of two tax slabs – 5% and 18%, along with a 40% demerit rate on sin, luxury, and demerit goods. The 2025 GST reforms were introduced to support students’ learning by reducing or exempting taxes on educational stationery products. Further, these Next Gen GST reforms also directly benefit cottage industries, artisans, MSMEs and supply chain stakeholders in the education sector.

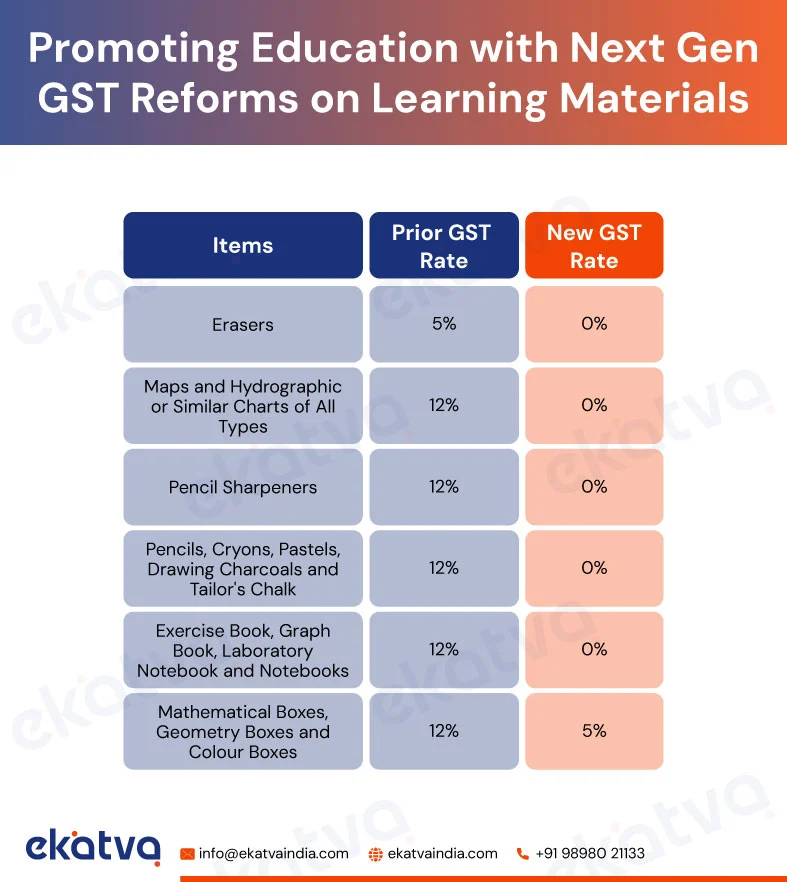

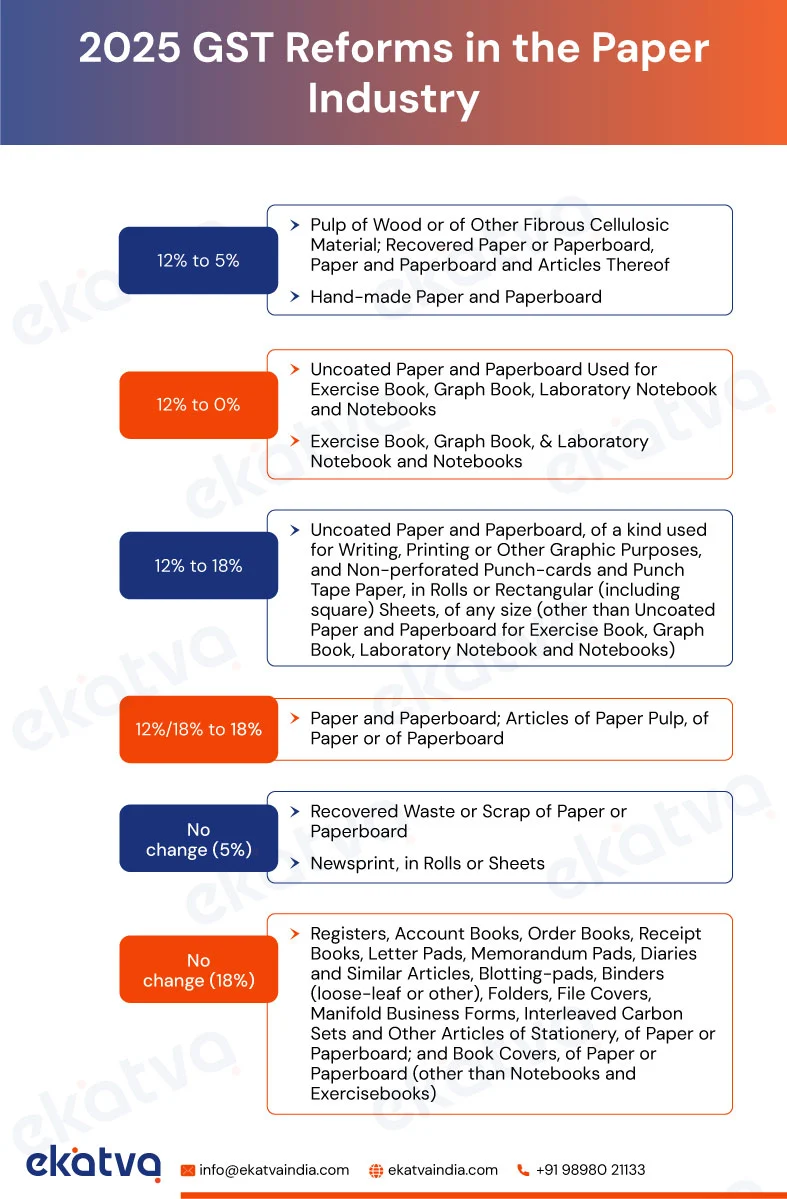

In the 56th meeting of the GST Council, Next-Gen GST reforms were approved, chaired by Smt. Nirmala Sitharaman, Union Finance Minister. The GST reform 2.0 exempts many educational stationery products from GST, such as graph books, pencils, erasers, pencil sharpeners, drawing materials, exercise books, printed maps, laboratory notebooks and globes. These products, primarily used for educational purposes, were previously sold at 12% tax, which has now been reduced to 0% tax.

The other stationery items, such as mathematical boxes, colour boxes, and geometry boxes, are subject to 5% GST from the 12% rate. Further, several changes were made in the paper industry as well; products such as paper or paperboard made of wood pulp or other fibrous cellulosic material were reduced from 12% to 5% GST rate. Other paper and paperboard, articles of paper pulp, of paper or of paperboard are now taxed at 18% from 12%/18% tax slabs.

Moreover, no changes were made to items of recovered waste or scrap of paper or paperboard, and newsprint, in rolls or sheets, remain at 5% GST rate. Also, other articles of paper, such as registers, order books, letter pads, account books, diaries, binders, file covers, book covers, manifold business forms and others, except notebooks and exercise books, continue to be taxed at 18% GST.

{kind=link}

Uncoated paper and paperboard used for printing, writing, or other graphic use, punch tape paper, and non-perforated punch-cards are taxed at 18% from 12%. Rest, GST rates reduced from 12% to 5% on handmade paper and paperboard.

However, certain challenges persist:

Uncoated paper and paperboards are categorised into three different GST rates (0%, 5% and 18%) based on the end use, which leads to an ambiguous interpretation for suppliers. An unclear understanding of what GST rates to apply may lead to penalties or reputational damage. This has created the need to maintain PO references or buyer declarations to validate the applied rates. Moreover, the same paper can be used for different means, so a customer may mislead the seller about the exact use. For instance, a customer purchases A4–size sheets for college work but uses them for printing purposes.

The best practice for suppliers is to get a written statement from buyers about the product’s use, or apply 18% GST when the use is unclear. Further, the suppliers should print the accurate HSN classification on invoices to apply accurate GST rates. The buyers, publishers, and notebook manufacturers should also maintain declarations, PO or inward registers to validate 0% GST purchases. These practices will help to deal with the above challenges and support the current GST reforms.

Still Confused with GST Paperwork in the Education Sector?

Leave your worries to us, and experience hassle-free GST compliance for your institution.